The GAAP Evolution: How Accounting Standards Evolved?

Introduction

In the intricate world of financial reporting, GAAP works as a common language for interpretation. Generally Accepted Accounting Principles (GAAP) serve as a cornerstone by providing a standard set of rules. These accounting guidelines help translate a company’s complex financial data into a universally interpreted narrative.

This article focuses on the evolution of GAAP over the years, from its origin to its contribution to establishing transparency in the financial world.

Origin of GAAP: From Chaos To Clarity

GAAP’s genesis sprouted from the persistent need for a standardized set of rules. With expanding economies and flourishing businesses worldwide, comprehending data and deriving accurate reports became complex. The stock market crash of 1929 served as a much-needed wake-up call, revealing the potential risks of manipulative financial reporting.

After this economic catastrophe, a set of principles emerged as a collective measure to regulate financial reporting. As a result, GAAP was formulated to establish accuracy in financial reporting and allow stakeholders to make well-informed decisions.

Evolution of GAAP in The United States

There are many key milestones that transformed the way GAAP worked in the United States. Let’s take a walk down the history and learn how GAAP evolved:

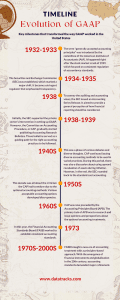

1. 1932-1933:

The term “generally accepted accounting principles” was introduced by the committee of the American Institute of Accountants (AIA). It happened right after the stock market crash of 1929, which focused on consistent regulation of accountancy standards.

2. 1934-1935:

The Securities and Exchange Commission (SEC) was established, which marked a major shift. It became a stringent regulator that emphasized transparency.

3. 1938:

To convey the auditing and accounting views, the SEC issued an Accounting Series Release. It aimed to provide a general perception of how financial reporting should be considered.

4. 1938-1939:

Initially, the SEC supported the private sector’s intervention in setting up GAAP. However, the Committee on Accounting Procedure, or CAP, gradually started publishing Accounting Research Bulletins. These bulletins served as a guiding path for the right accounting practices to be followed.

5. 1940s:

This was a phase of various debates and diverse thoughts. CAP continued issuing diverse accounting methods to be used in varied practices. During this period, there was also a discussion about using upward revaluation of assets during inflation. However, in the end, the SEC rounded back to the standard cost accounting.

6. 1950s:

This decade was all about the criticism the CAP had to endure due to the optional accounting methods. Various acceptable accounting options developed discrepancies.

7. 1960s:

CAP was now preceded by the Accounting Principles Board (APB). The primary task of APB was to research and issue opinions and perspectives about the optional accounting treatments.

8. 1973:

In this year, the Financial Accounting Standards Board (FASB) worked to establish consistent accounting standards.

9. 1970s-2000s:

FASB brought a new era of accounting treatment with a principles-based approach. With the emergence of financial instruments and globalization in the 20th century, accounting standards demanded major refinement.

10. Beyond 2000s

It was evident that GAAP underwent a remarkable transformation by the dawn of the 21st century. From the consistency-based approach to principles-based standards, it has witnessed rounds of changes.

However, GAAP has become a significant tool in checking transparency and regulating the accountability of the financial landscape.

Why GAAP Compliance is Much Needed?

Trust becomes the crux of the matter in the precarious world of finance. From stakeholders to investors, everyone relies on financial statements to make decisions. That’s when GAAP emerges as a mark of transparency. It fosters a safe ecosystem for businesses, ensuring trust and accountability.

Below are a few reasons why GAAP compliance matters:

Assist in Well-Informed Decision

Investors and creditors can easily check a company’s financial health. GAAP provides a standardized approach to financial analysis, leading to sound financial decisions.

Establishing Trust and Credibility

Financial statements prepared in compliance with GAAP have a standardized and universally accepted format. Companies that follow GAAP show their commitment to trust and accountability.

Minimize Risk and Maximize Efficiency

A standardized approach to accounting reduces inconsistencies, thereby mitigating the risk of errors. Additionally, the use of the GAAP framework enhances a company’s internal efficiency by saving its time and resources.

Takeaway

At DataTracks, we offer a suite of data-driven solutions for the regulatory reporting process. From simplifying data collection to ensuring accuracy, we take care of everything. With DataTracks by your side, you can focus on what matters the most for your business.