The XBRL Juggernaut – The Role of Singapore’s Regulators

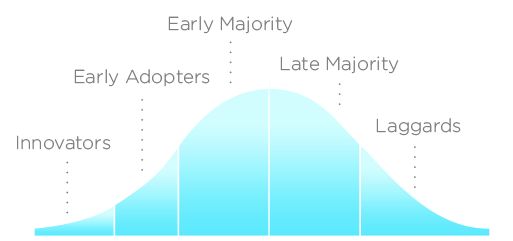

Every technology has an adoption lifecycle as described in the famous ‘diffusion of innovations’ theory. The theory states that the sum total of all the adopters of a technology (say Tech A) can be represented by the area under a bell curve.

This total area can be divided into five parts based on the adoption of the XBRL technology:

- Innovators

- Early Adopters

- Early Majority

- Late Majority

- Laggards

From Wikipedia (edited)

As far as XBRL technology is concerned, Singapore would easily fall in the early adopters bracket. They were not adventurous innovators like the Tokyo Stock Exchange in Japan (TDnet) and the FFIEC in the US (Call Reporting). However, considering the number of data collection regimes across the world that are yet to adopt XBRL as a superior data standard to incumbent methods and technologies, its adoption by Singapore’s Accounting and Corporate Regulatory Authority puts them in the early adopters category fairly easily.

Technology adoption is subject to network effects. So the more the number of parties that adopt XBRL, the more benefit each party derives. All-purpose analytics tools can be developed and used with minor tweaks, thus compressing implementation timelines. Much simpler (and I dare say, much more efficient) compliance reporting systems can be deployed. All of this will happen because of a thriving ecosystem of vendors and clients for compliance and analysis software and services.

Singapore Regulators Encourages adoption of XBRL Technology

The adoption of XBRL is, in effect, inexorable. Therefore, all of Singapore’s regulators (and, in fact, data collectors) would do well to look at XBRL as a long-term solution to data collection, handling and processing.

There have been some very encouraging signs. Singapore’s interest in the Solvency II third-party equivalence program implies a forward-looking mindset among the powers that be, as far as the insurance standards are concerned. A similar mindset may realistically be hoped for in terms of the transition to XBRL as well.

XBRL is no longer the early-stage, unproven data upstart it once was. It’s time the world recognized it as a technology that has made it.

About DataTracks:

DataTracks is a global leader in preparation of financial statements in XBRL and iXBRL formats. With over 10 years’ experience, DataTracks prepares more than 12,000 XBRL statements annually for filing with regulators such as SEC in the United States, HMRC in the United Kingdom, Revenue in Ireland, ACRA in Singapore and MCA in India. DataTracks provides world-class services with its team of certified accountants experienced in US GAAP, UK GAAP, India GAAP, SFRS and IFRS.

The views expressed are that of the author’s and DataTracks is not responsible for the contents or views expressed therein. If any part of this blog is incorrect, inappropriate or violates the IP rights of any person or organization, please alert us at ceo@datatracks.com. We will take immediate action to correct any violation

To find out more about DataTracks, visit www.datatracks.com/sg/ or send an email to enquiry@datatracks.com.sg